Why Businesses Choose Our 401(k) Plan Guidance

As a 3(21) advisor, Konza Global Wealth Group provides fiduciary investment guidance grounded in transparency, unbiased advice, and ongoing support, helping businesses stay aligned with their financial goals.

Our Advantage

Discover the advantages of partnering with a team that champions your employee and firm objectives.

As a 3(21) advisor, we offer distinct advantages that benefit our clients seeking prudent investment guidance with fiduciary responsibility:

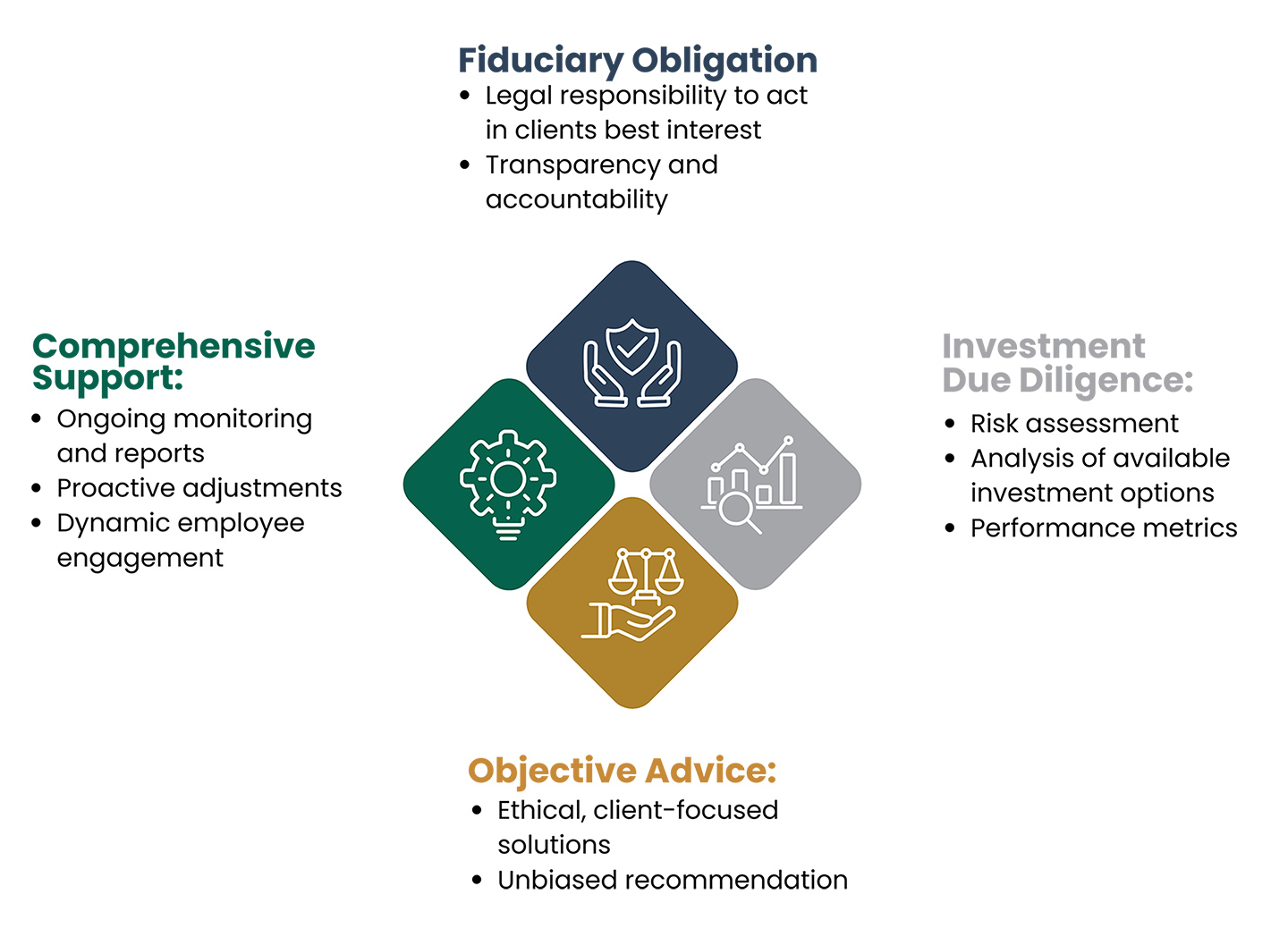

Fiduciary Obligation:

- Legal responsibility to act in clients best interest

- Transparency and accountability

Investment Due Diligence:

Investment due diligence helps employers review risk, investment options and performance metrics as part of ongoing plan oversight.

It should also connect with plan structure and fee review so employers can evaluate costs, monitoring processes and overall plan design together.

- Risk assessment

- Analysis of available investment options

- Performance metrics

Objective Advice:

- Ethical, client-focused solutions

- Unbiased recommendation

Comprehensive Support:

- Ongoing monitoring and reports

- Proactive adjustments

- Dynamic employee engagement

Working with Konza Global Wealth Group

Clients benefit from professional investment manager selection, fiduciary oversight and objective guidance that supports broader business retirement plan services.

For additional educational context, review how to choose the best 401(k) plan for your employees.

Tell us your financial aspirations, and we’ll handle the rest

Our team actively manages your portfolio using tailored strategies that maximize returns and minimize risk — providing you with reports and insights every step of the way.

Frequently Asked Questions

Why Should Employers Review 401(k) Plan Fees and Fiduciary Support?

Employers should review 401(k) plan fees, investment options, monitoring practices and fiduciary support to help keep the plan aligned with employee needs and business goals. Regular review can also help identify gaps in cost structure, investment due diligence, reporting and plan oversight.

For related planning context, review our plan structure and fee review guidance and broader business retirement plan services.

What Does a 3(21) Advisor Do for a 401(k) Plan?

A 3(21) advisor provides fiduciary investment guidance for a retirement plan while helping employers review investment options, risk, performance and plan oversight needs. The plan sponsor still keeps decision-making authority, but the advisor supports more informed fiduciary decisions.

Why Is Investment Due Diligence Important for Employers?

Investment due diligence helps employers review available investment options, risk levels, fees, performance metrics and whether plan choices still align with participant needs. This process can support better plan oversight and stronger long-term retirement outcomes for employees.

How Does Fiduciary Support Help Business Owners?

Fiduciary support helps business owners understand their responsibilities when offering a retirement plan. It can also support investment monitoring, documentation, reporting and objective plan guidance.

Why Do Employers Need Ongoing 401(k) Plan Monitoring?

Ongoing 401(k) plan monitoring helps employers review investment performance, employee engagement, plan costs, reporting needs and possible changes in plan strategy. Regular monitoring helps keep the plan aligned with business goals, employee needs and fiduciary expectations.

How Can 401(k) Plan Guidance Support Employees?

401(k) plan guidance can support employees through better investment education, clearer plan communication and stronger retirement planning resources. This can help employees understand their options and make more confident decisions about long-term savings.